Loan Application Process Demystified

Navigating the loan application? This guide simplifies the process, offering insights for a successful borrowing experience.

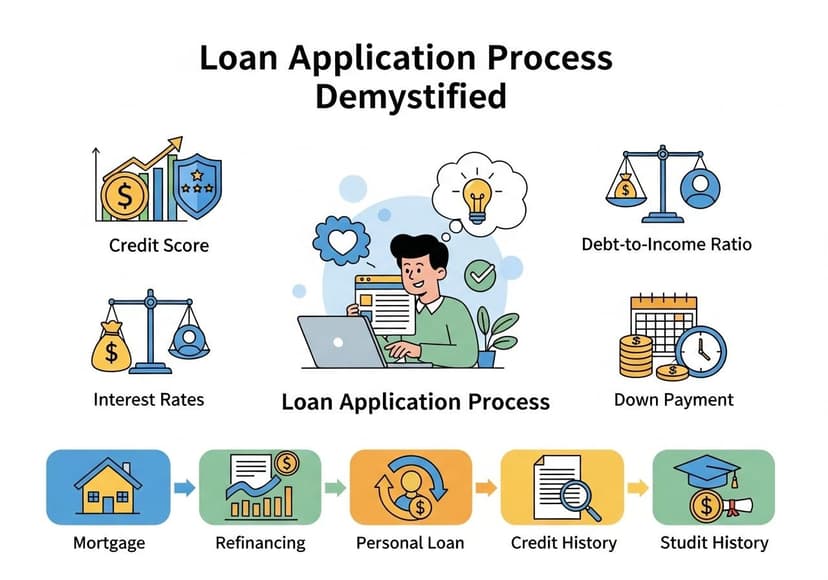

The Basics of the Loan Application Process

Stepping into the world of loans can seem daunting, especially for first-time borrowers. The Loan Application Process involves several critical steps that determine whether your application will be successful. This guide aims to simplify the process, paving the way for a clearer understanding of what to expect. Getting familiar with terms like Credit History, Credit Score, and others will empower you to tackle your loan application confidently.

Understanding Credit History

Your Credit History is a report card of your borrowing behavior over time. Lenders utilize this history, which includes your Credit Score, to assess your reliability as a borrower. The better your credit history, the more favorable terms you can secure, such as lower Interest Rates. Managing your credit responsibly can significantly impact your loan approval chances, making it essential to stay informed and proactive.

What Is a Credit Score?

Your Credit Score is a three-digit number that summarizes your creditworthiness based on your history of borrowing and repayment. Scores typically range from 300 to 850; higher scores indicate a lower risk for lenders. Before applying for a loan, it can be wise to check your score. If your score is less than stellar, consider improving it by paying down debt or correcting errors on your credit report.

Evaluating Your Debt-to-Income Ratio

Another significant factor in the loan process is your Debt-to-Income Ratio (DTI), which compares your monthly debt payments to your gross monthly income. Lenders often look for a DTI below 36%. A higher ratio could result in a denied application or unfavorable loan terms. Before applying, take a moment to assess your DTI and consider adjustments if necessary.

Types of Loans Available

There are various loans available, ranging from Personal Loans to Mortgage options. Each type has its unique requirements. For instance, a mortgage typically requires a substantial down payment and a long loan term, while a personal loan may offer more flexibility in amounts and terms.

If you're a student seeking financial aid, Student Loans are tailored specifically for you, often with lower interest rates. Always consider your options, and if you're unsure, consulting with a financial advisor can help maneuver through the plethora of choices.

Understanding Down Payments and Loan Terms

Most loans require a Down Payment, which is a portion of the total loan amount you pay upfront. The size of your down payment can affect your loan’s overall cost, directly influencing your monthly payments and Interest Rates. Additionally, the Loan Term refers to the duration over which you will repay the loan. Shorter terms often come with higher monthly payments but less interest paid overall.

The Role of a Cosigner

If your credit isn’t optimal, you may want to consider having a Cosigner. A cosigner is someone who agrees to take full responsibility for the loan if you cannot repay it. This can greatly improve your chances of approval, as lenders see a responsible cosigner as a safety net in case of default. Remember, this is not a decision to take lightly; both parties need to fully understand the responsibilities involved.

Refinancing: A Smart Financial Move

Once you're caught in a loan, you might find yourself considering Refinancing as a way to secure lower interest rates or improved loan terms. Refinancing can potentially save you money in the long run, freeing up funds for other investments or savings. Just ensure that the costs of refinancing do not outweigh the benefits; this is where your Credit History will play a significant role again.

Where to Start: Essential Resources

Having the right resources by your side is crucial. For healthcare professionals looking into loan repayment, you can check out the services offered by Nurse Corps Loan Repayment. If you are a business owner dealing with disaster-related financial burdens, make sure to review the assistance offered by the SBA Disaster Assistance program.

Final Thoughts

The Loan Application Process does not have to be a mystery. By understanding your Credit History and preparing ahead of time with knowledge on Credit Scores, Interest Rates, and more, you can navigate this journey with confidence. Each step brings you closer to securing the financing you need, whether it’s for a mortgage, a personal initiative, or educational purposes. Happy borrowing!

Related Posts

21 Month 0 Percent Balance Transfer Offer

Enjoy 21 months without interest, helping you manage debt and save on interest charges.

Best Accounting Software For Mac

Good accounting software streamlines finances, offering efficient tracking, reporting, and management for businesses effectively.

Best No Annual Fee Credit Cards To Consider

Explore top-tier credit cards without annual fees, offering valuable rewards and benefits, ideal for smart spending.